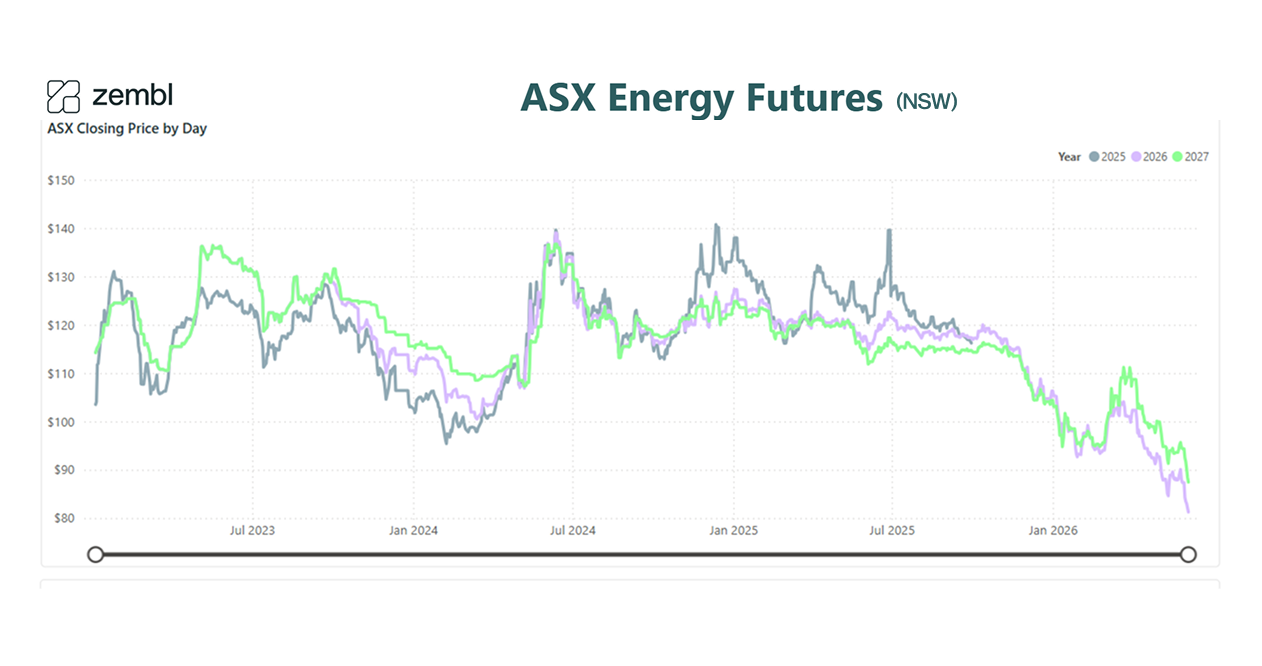

May delivered a decisive slide in wholesale electricity futures as winter demand remained tepid and battery storage continued to reshape market dynamics. ASX futures for 2026 delivery fell from around $89.50 early in the month to $82.12 by month end¹, a significant eight-week low, while 2027 contracts held firm in the $88–94 range, signalling market caution around near-term supply.

Why prices kept sliding

Winter typically brings peak demand, but May's cooler conditions across eastern Australia failed to drive the seasonal lift. Cold snaps were scattered rather than prolonged, and mild stretches in between kept heating demand muted. The result: wholesale prices continued the downward path established in April, with every mainland state tracking lower through the month.

What's happening in the NEM

Batteries are now the default price-maker across the grid. With battery storage capacity north of 30 GW in development², the grid is seeing fewer high-price spikes during evening peak. Instead, batteries absorb off-peak and daytime solar generation, then discharge during peak, capping wholesale prices far more effectively than gas peakers did a year ago⁵. This is great news for grid stability and brutal for gas generators. Coal retirements continue on schedule, yet the grid isn't tightening; renewables and storage are filling the gap faster than anyone expected.

May's data reinforced the trend: no state saw sustained price rallies, and NSW typically the strongest region, traded only modestly above Queensland and Victoria³. South Australia, with its high solar penetration, stayed at the lower end of the band.

What to watch

Next 3 months: June and July will test whether winter finally bites. If cold snaps hit hard, gas will get a look-in and prices could spike. If conditions stay mild, 2026 contracts could remain soft. Watch 2027 contracts closely as they're trading $6–8 above 2026, hinting that the market sees near-term softness but expects tighter conditions in year two.

Next 6 months: New battery capacity coming online (another 5–8 GW expected by end of year) will further suppress peak prices. Solar installations are accelerating into spring and summer. The question is whether demand-side management and grid services pricing can support enough renewable investment to maintain stability when coal units do retire.

Next 12 months: The major unknown is network tariff reform. If new cost-reflective tariffs roll out as planned⁴, demand patterns will shift, potentially flattening peaks and widening pricing bands. That's value back to efficient operators and a genuine test for businesses with fixed-time contracts.

The takeaway

May was the month the wholesale market accepted that 2026 will be softer than 2025. Prices fell sharply, 2027 contracts held steady, and the reason is clear: supply is abundant and demand isn't desperate. For businesses with contracts expiring in the June–August window, this is a genuinely attractive entry point, but the 2027 premium suggests conviction that supply will tighten soon. The risk of waiting is real; the reward of locking in now is tangible.

Sources

- ASX Energy Futures (NSW) closing price data, May 2026: https://www.asxenergy.com.au/

- AEMO – Battery storage in development across the NEM (30+ GW): https://www.aemo.com.au/

- ASX Energy Futures (NSW) closing price data, May 2026: https://www.asxenergy.com.au/

- AER – Cost-reflective network tariff reform roadmap 2026: https://www.aer.gov.au/

- Utility Magazine – Battery revenue records and grid service pricing: https://utilitymagazine.com.au/

.png)

.png)

.png)

.svg)