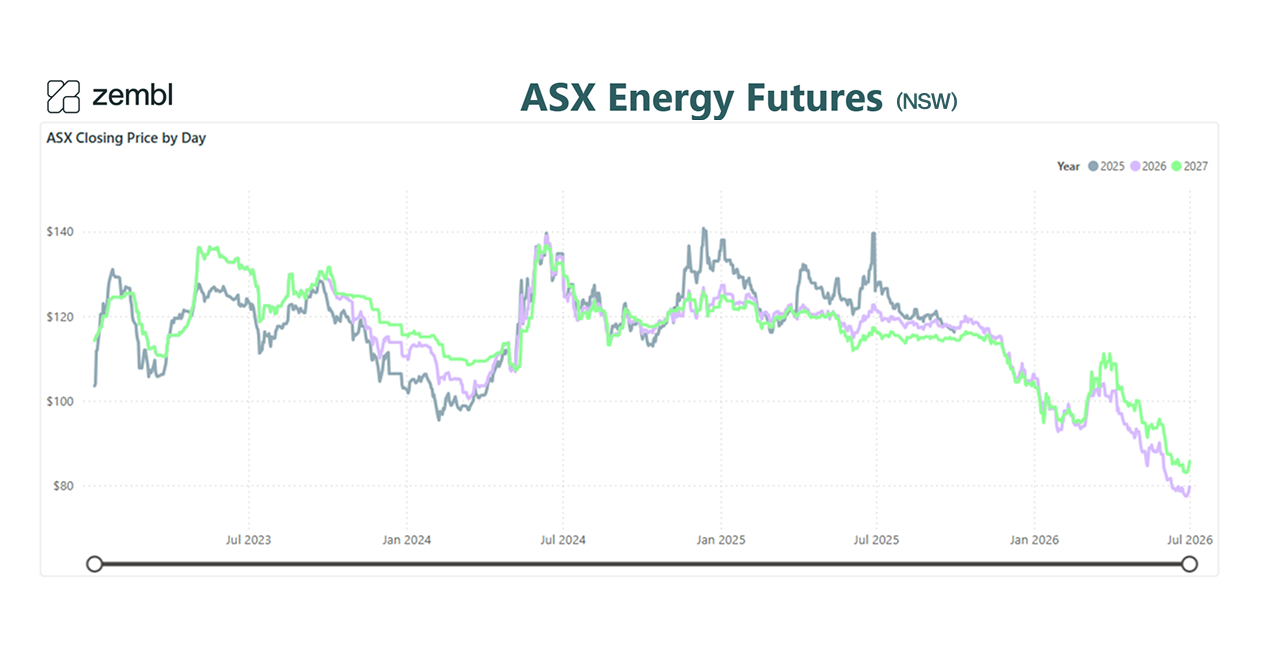

June showed little sign of the expected winter's bite with demand remaining muted. Across NSW, wholesale electricity futures for 2026 dropped from $84.29 at the start of the month to $78.51 by month end¹, marking it the lowest point since the start of 2025 – a trend mirrored across every mainland state. More tellingly, 2027 prices compressed from $92.46 down to $84.26, narrowing the year-on-year premium to just $5.75.

Why a mild start to winter is delivering better prices

June 2026 delivered scattered cold snaps and mild stretches in between, with no sustained freeze to push heating demand - that could push up wholesale prices. Across eastern Australia, the grid coasted, load managers had breathing room, and gas generators did not see the uptick in demand that can come when temperatures suddenly change. With low urgency from the demand side and consistent supply streaming in from renewables and battery dispatch, consumers saw a month that did not meet high price expectations.

What's happening in the NEM

Batteries are now a key price-setter during the evening peak. With 30+ GW in development across the NEM², the grid is awash in off-peak and daytime solar generation that is stored and dispatched during the evening peak. Gas generators – traditionally the key price setter during high-demand windows – are facing competition. Coal retirements remain on schedule, yet the grid isn't tightening yet.

June's data reinforced this consistently: no state saw expected price increases, and NSW – typically the higher cost region – traded only modestly above Queensland and Victoria³. South Australia, with its high solar footprint, stayed at the lower end of the band. The current 2026 price decline was mirrored across every mainland state.

What to watch

Next 3 months: July and August will be the final test of winter demand. If a cold snap finally hits, gas might get a look-in and prices could spike. With 2027 prices trading only $5.75 higher than 2026 – it is a signal the market appears to no longer expect supply to tighten significantly next year.

Next 6 months: New battery capacity coming online (another 5-8 GW by end of year) will likely impact peak prices. Solar installations continue to accelerate. The question is whether grid services pricing and demand-side management can support enough renewable investment when the next tranche of coal retirements lands. Storage economics are promising, however, the grid's ability to monetise them through firm capacity payments is not yet proven.

Next 12 months: Network tariff reform remains the major unknown. If cost-reflective tariffs roll out as planned⁴, demand patterns are expected to shift - potentially smoothing out some daily price swings while giving customers greater pricing and product choices. That's genuine value for efficient operators and a real test for businesses locked into fixed-time contracts.

The takeaway

June was the month where a warm start to winter meant 2026 is softer than 2025 year to date. Prices fell sharply, 2027 future prices softened, and early winter demand simply not materialise.

For businesses with contracts expiring July-September, now remains an attractive entry window. It is worth considering that prices move up, and down. The current run of lower pricing is a key opportunity to secure lower than expected rates across 2026 out into 2029.

Sources

- ASX Energy Futures (NSW) closing price data, June 2026: https://www.asxenergy.com.au/

- AEMO - Battery storage in development across the NEM (30+ GW): https://www.aemo.com.au/

- ASX Energy Futures (NSW) closing price data, June 2026: https://www.asxenergy.com.au/

- AER - Cost-reflective network tariff reform roadmap 2026: https://www.aer.gov.au/

- Utility Magazine - Battery revenue records and grid service pricing: https://utilitymagazine.com.au/

.png)

.png)

.png)

.png)

.svg)